Q4 2025 Market Outlook: Bridge Lending Opportunities

Executive Summary

Bridge lending is not just holding steady—it’s accelerating into Q4 2025. The gap left by banks is widening, deal velocity is climbing, and private lenders with the ability to move fast will dominate in the year’s final quarter.

Why Bridge Lending Is Set to Surge in Q4 2025

- Banks Are Out of Position

Credit committees are still stuck in slow-motion. That’s leaving profitable, time-sensitive transactions on the table—transactions private lenders can close in days, not months. - Year-End Deal Rush

Institutional buyers, developers, and opportunistic investors are pushing to close before the calendar flips. For borrowers facing a hard deadline, bridge capital is the only viable option. - Refinancing Wave

A wall of CRE and multifamily debt is maturing before year-end. Bridge lenders who step in to cover the gap will lock in premium yields and strong collateral positions.

Where the Action Is

- New York – The largest and most competitive bridge market in the country. High-value multifamily and mixed-use assets demand rapid execution.

- Dallas–Fort Worth – Massive deal flow in industrial and multifamily. Developers are already lining up capital for Q1 2026 starts.

- Miami – Red-hot residential demand paired with investor migration is fueling acquisition and repositioning deals.

- Phoenix – Land and redevelopment plays are back in focus with attractive entry pricing.

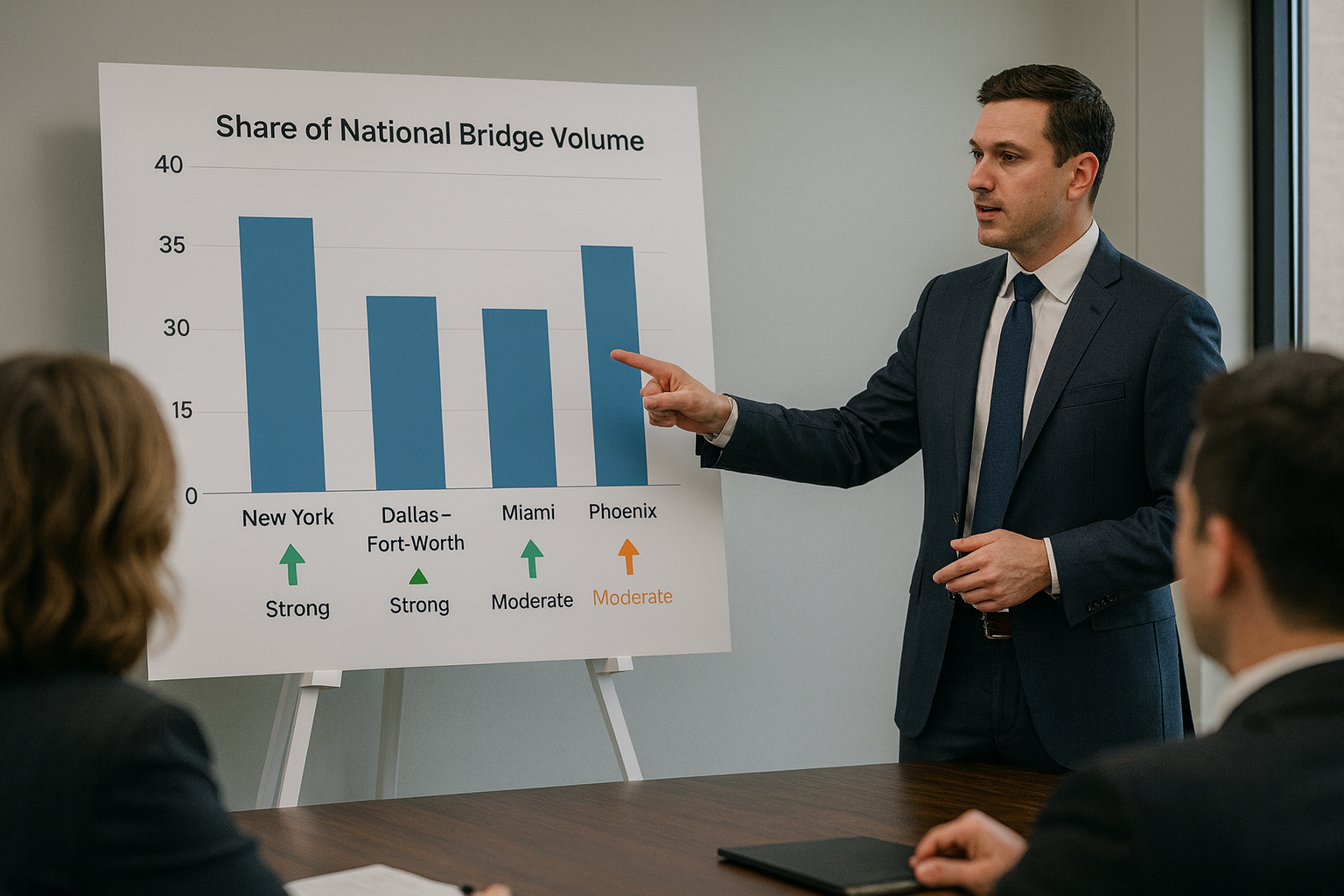

Lending Activity Snapshot

Based on 2025 year-to-date deal data:

| Metro | Share of National Bridge Volume | Trend vs. 2024 |

|---|---|---|

| New York | 38% | ▲ Strong |

| Dallas–Fort Worth | 25% | ▲ Strong |

| Miami | 18% | ▲ Moderate |

| Phoenix | 14% | ▲ Moderate |

Why Q4 2025 Will Be a Lender’s Quarter

- Pricing Power – Limited competition from banks means lenders can dictate terms.

- Premium Collateral – Borrowers with serious assets are coming to the table.

- Repeat Business Pipeline – Deals closed now are feeding into 2026 refis and exits.

The Playbook for Winning Deals

- Move from signed term sheet to close in under 10 days.

- Maintain disciplined LTV and underwriting standards.

- Focus on borrowers with a proven track record and a clear exit.

Bottom Line:

Q4 2025 is not a “wait and see” quarter—it’s a take-the-market quarter. Lenders who hesitate will miss the best spreads and the cleanest deals of the year.